The UK ad market grew 6.4% last year. Congratulations to Google, Meta, and Amazon.

““Fantastic to see the evolution of the AA/WARC Expenditure Report and such positive projections for our industry.”

That was the laudatory view of the UK’s trade association for ad agencies, the IPA, after the latest Advertising Association/WARC Expenditure Report revealed UK adspend had grown by 6.4% to £46.7bn last year.

It certainly seems “fantastic”, doesn’t it? Then, why, as I asked in my Media Leadercolumn yesterday, are most people in advertising so gloomy these days? Wasn’t it only three months ago that we were being told there is a market “exodus”, with jobs being disappeared amid the AI automation revolution?

Or maybe this idea of adspend ‘growth’ is “fantastic” in the more literal sense. Namely: it’s becoming a polite fiction to mask what’s really happening.

Indeed the stories that matter in recent days come from the most obvious of sources: Big Tech companies’ latest earnings results.

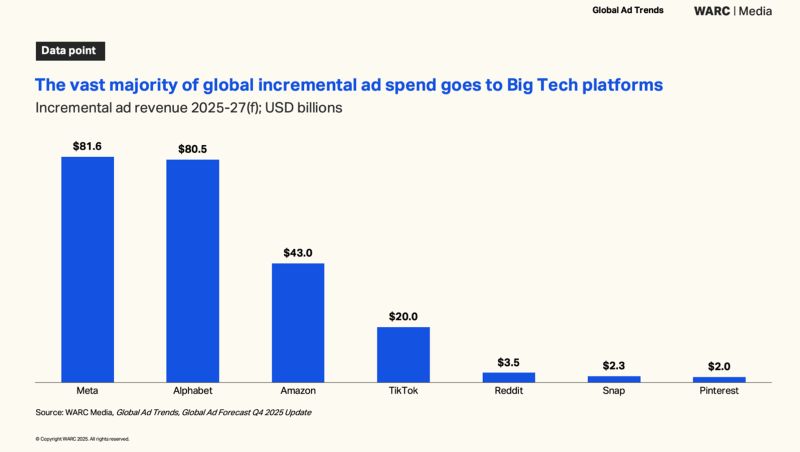

Alphabet: 22% year-on-year revenue growth in Q1 to $109.9bn.

Meta: 33% year-on-year revenue growth to $56.3bn.

Amazon (advertising business): grew 24% year on year to $17.2bn.

I used to religiously cover these earnings nearly a decade ago as a tech editor for Campaign, and I still ask myself the same question today as I did then: “How can these already huge companies still grow so quickly?”

If you were paying attention, as Press Gazette was last week, you’ll know it’s because what used to be an “advertising industry” is now a sharing of the spoils between these three companies, which collectively pull in 2 of every 3 pounds spent on UK advertising services. That’s just £15bn for the rest.

The real numbers

This is not just a UK phenomenon.

In WARC’s Global Ad Trends Report: Media’s New Normal, which I co-authored last December, we featured a number of data points which lay bare how a headline adspend growth figure doesn’t begin to tell you what’s now happening in our industry.

In fast-growing ad categories — clothing, electronics, cross-border e-commerce — almost 80% of incremental spend now flows directly into retail media, paid search, and social platforms. The remaining 20% is shared across the entire rest of the media industry. Everything. TV, audio, publishers, out-of-home, the lot.

UK advertising spend on low-attention media has risen from 32% of total investment in 2015 to 70% in 2025. High-attention media — the environments where advertising actually builds brands — has gone from 68% to 30% in the same period.

So the industry is spending more money, in worse environments, for thinner results.

And 80% of campaigns achieve their reach potential. Only 25% achieve their effectiveness potential. The industry is measuring the thing that’s easy to prove, not the thing that matters. This is not a healthy market. It is a market that has learned to describe itself as healthy using metrics that can’t see what’s wrong with it.

The ruler problem

I’ve argued before that measurement is never neutral; it reflects the interests of whoever holds it. The platforms built attribution models that credit themselves. The dashboards that govern performance budgets were designed by parties with skin in what those dashboards conclude.

Of course we need reports like AA/WARC to give us some idea of where the money’s going. But the story that really matters is not the headline number that seems ‘fantastic’.

As we explained in Media’s New Normal, there is a new-wave of digital-native budgets in advertising that have little connection to household spending power. SMEs, trade-marketing funds, retail media networks, as well as certain tech and electronics verticals, are pouring billions into digital ecosystems that promise accountability and speed.

Importantly, they optimise for performance, not reach. Their budgets were born in search, social and retail media – and, so far, they’ve stayed there. They favour environments that can demonstrate immediate results, not channels that build long-term brand equity.

Focusing on a headline number, therefore, blinds us from the two-speed system that is only getting starker: legacy categories whose spend is broadly stable, and new categories whose explosive growth flows disproportionately to the major platforms.

When you control what gets counted, you control what gets funded.

The rational choice

The most important question isn’t why the industry produces flattering headlines. It’s why senior practitioners keep accepting them.

Most people reading this have sat in a room where someone presented a version of the 6.4% figure as evidence of a robust market, while privately knowing that their publisher client’s revenues are declining, that their independent agency is being squeezed, that the incremental budget they’re fighting for this quarter is going to Meta’s self-serve platform before it ever reaches them.

The knowledge is there, but so is the seductive power of the happy-clappy narrative. Questioning the frame means questioning the clients, the platforms, the trade bodies, and the data infrastructure that everyone has built their businesses around. It means telling a board that the market you claimed expertise in is consolidating in ways that structurally chip away your relevance. It means accepting that two decades of decisions — about programmatic adoption, platform dependency, measurement infrastructure — contributed to the number you’re now hoping nobody looks at too closely.

That’s an expensive conversation to start.

So the 6.4% gets cited at conferences. It goes in new-business decks. It provides comfort to people who need comfort. And next year the number will be slightly different, the £31bn will be slightly larger, and the methodology may quietly change again.

The question isn’t whether you know what’s really happening. It’s what you’re planning to do about it.

This article first appeared in Ad-verse Reactions, a newsletter written by independent journalist and consultant Omar Oakes, covering the economics, power structures and unintended consequences shaping advertising and media. You can subscribe to Ad-verse Reactions for regular analysis at omaroakes.substack.com.

This article first appeared in Ad-verse Reactions, a newsletter written by independent journalist and consultant Omar Oakes, covering the economics, power structures and unintended consequences shaping advertising and media. You can subscribe to Ad-verse Reactions for regular analysis at omaroakes.substack.com.