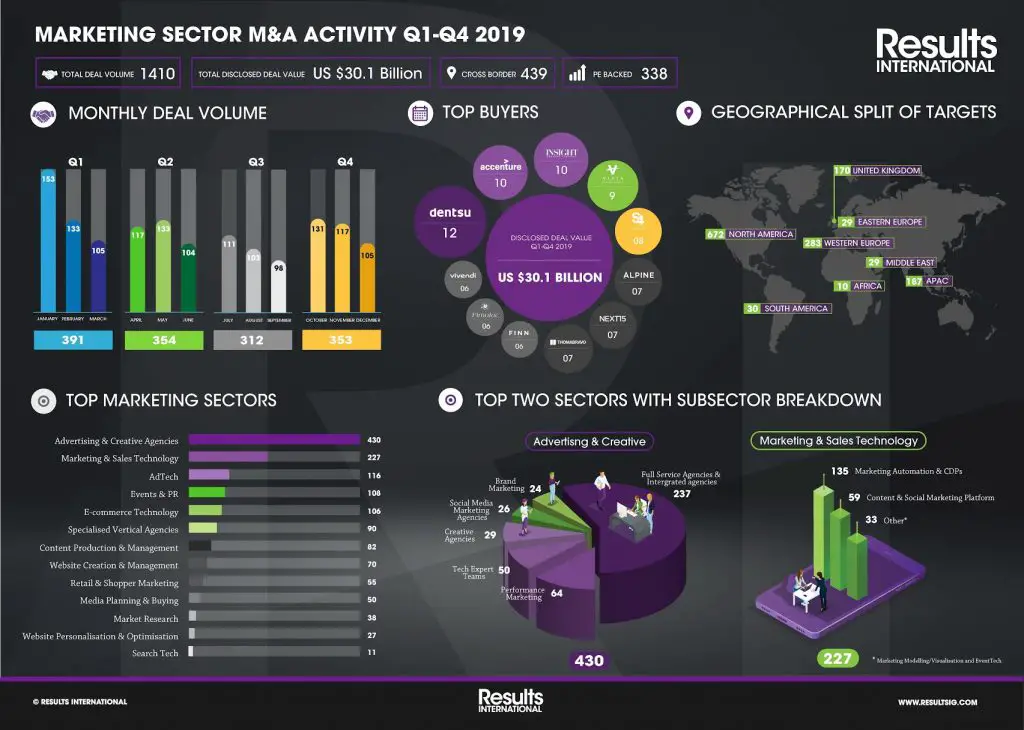

The agency holding companies are in full retreat in the mergers and acquisitions (M&A) stakes according to new figures from Results international and marketing consultancy R3.

According to Results, while Publicis did the biggest deal in the first half of 2019 with its $4bn buy of data firm Epsilon, by volume private equity companies accounted for about half of all deals. PE firm Insight Venture Partners was the most acquisitive in H1 completing eight deals.

Dentsu was the most active of the agency groups with six. In the same period last year it made 17. WPP, for long the most active buyer under Sir Martin Sorrell, abandoned the field although that may now change as it stands to receive £2.5bn from the sale of 60 per cent of research business Kantar to Bain Capital.

Accenture swum against the tide with three more traditional creative buys (most of the other sales were digital specialists): Droga5 and Shackleton in April and PXP/X in June.

Results partner Julie Langley says: “Private equity has been a key driver in marketing industry M&A for some time now, as PE buyers are excited by the transformative change and subsequent growth of agencies that are leading change in the sector.

“The ‘buy and build’ approach PE takes has led to the creation of many new PE-backed agencies with exciting new capabilities focused on future / next generation marketing. They, along with new entrants including the likes of LinkedIn, Apple and Walmart, are keeping the market vibrant, as many of the traditional network buyers focus their attention internally. These acquirers are recognising that the ability to identify customers individually and provide them with targeted and personalised marketing is a key driver to increasing sales.

“Agencies that have the technology, creative ability, talent and capabilities to manage and deliver this personalised approach to marketing at scale are in high demand.”

From the other side of the Atlantic the view is much the same. Consultancy R3 says $13.6bn was invested in the marketing services industry in the first half of 2019 – a 43 per cent increase over the same period in 2018 – across 235 deals.

Co-founder and principal Greg Paull says: “North America and martech are holding up the M&A market as buyers look for as much certainty as they can get. It’s a scramble for first-party data, and the increased valuation and spend on martech companies reflect that value.

“The high rollers of marketing M&A continue to be consultancies, private-equity groups and technology companies. Holding companies have their focus elsewhere as they urgently need to work out new business operating models as consultancies edge into the industry and in-housing grows in popularity with clients.”

Top 10 Buyers in 1H 2019 – R3

1/Publicis Groupe ($4.4bn)

2/Accenture ($651m)

3/CVC Capital Partners

4/Dentsu

5/Stagwell Group

6/Cision

7/DMI

8/CM Group

9/Deloitte

10/Hexaware Technologies