The pandemic has delivered human, social, and economic costs across the world which will affect us for years to come. According to YouGov, UK consumer confidence has sunk to its lowest level since 2012 and 86 per cent of people surveyed believe we are headed towards a depression or recession. While the scale of damage that Covid-19 has created likens it to the 2008 financial crisis, the pandemic has unfolded differently for consumers and the financial sector.

For consumers, the pandemic and subsequent lockdown represent a dangerous, but slow moving and unclear threat. The risk the virus poses is prominent in our lives and we feel we will be contending with it for most of 2020. 56 per cent of the UK public expect the virus to be in the UK for more than 6 months, with 82 percent believing it will exist globally for the same period (YouGov).

Economically, it has an enormous, dominant effect on what we buy, when we buy it and why. But we have yet to work out how badly it will affect us as a nation. The lockdown has created an environment where we know we need to try and safeguard our financial health, but we don’t have clear actions in the same way we did to safeguard our personal health by staying at home. According to IPSOS, only 23 per cent of the UK public want to restart the economy and a sizeable percentage of the population are nervous about returning to work, jobs, and public transport.

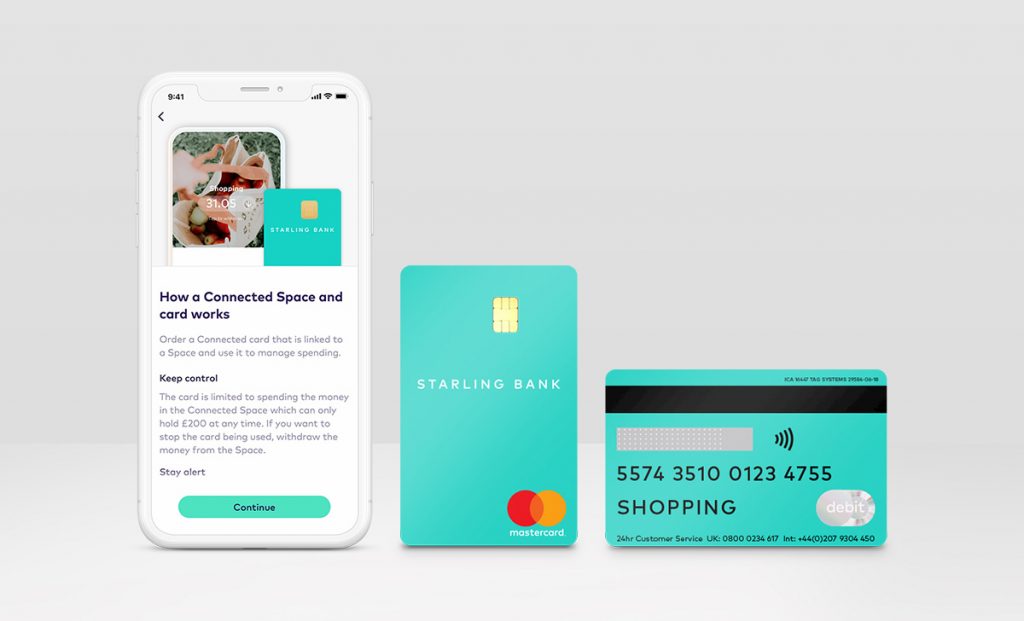

In the face of this uncertainty, the financial sector has an opportunity to rethink their relationship with consumers and become a champion of recovery. As the pandemic has unfolded, we have already seen financial brands engaging in traditional ways, such as government backed plans, and non-traditional ways, such as new products and offerings. For example, connected or volunteer cards, which allow NatWest or Starling Bank customers to request an additional, specially restricted payment card that can be given to vulnerable friends or family have shown how banks can address indirect financial issues through innovation.

Despite challenges in delivering support at scale, banks are being perceived as handling the pandemic positively, with 50 per cent of the UK population approving of their efforts and another 31 per cent neutral (GWI). Maintaining this level of support will require going beyond current efforts in the days and weeks ahead. As consumers move out of lockdown to rebuild their lives, businesses attempt to reopen and government support schemes have variable extensions, the financial damage we have yet to fully realise will be felt.

The financial sector must return to its raison d’etre: providing financial security, availability and guidance. However, in the face of the pandemic, it must think about how to deliver this in new ways. Just as the UK population took extraordinary measures to ensure our collective safety, so must our institutions.

For consumers, this means rethinking payments, loans, products and staff engagement. It requires going beyond a transactional relationship to becoming an advocate – helping not just to advise on financial issues but fighting for them at scale with the government and other sectors. From securing the basics such as safety and our homes, to helping restore and rethink our long-term financial plans, banks are going to have to rethink their role in our lives, just as we rebuild them. It is not enough to talk about their customer’s financial health, they need to look after everyone with wider reforms which could come from collective innovation in mortgages, rent and duties.

For businesses, banks need to become a source of support beyond the financial. Businesses that have survived the pandemic reopen to uncertain times. Nervous consumers, changing purchase behaviours and the possibility of new outbreaks mean the ability to open doesn’t necessarily mean a smooth path back to growth. Beyond new ways to loan and fund, banks need to help use their scale, insight, and base to provide a pipeline to get customers back in the door. The death of the high street and the contraction of many UK business verticals is not the sole responsibility of the financial sector to fix. But in our current situation they might be the only ones who can.

The pandemic and the recession that will come after it may seem like a replay of the 2008 crash, but this time we can find salvation in a sector more used to being blamed. As long as banks realise that we are all in this together.

DuBose Cole is head of strategy at VaynerMedia London.

DuBose Cole is head of strategy at VaynerMedia London.